Exploiting Creditor Agreements for Control and Profits

How distressed debt investors attempted the "J. Screw" on Serta Simmons Bedding.

In March 2020, $2 billion of Serta Simmons Bedding’s first-lien loan crashed to 39 cents on the dollar. Sensing the opportunity, a coalition of distressed debt investors led by Apollo (with participation from Angelo Gordon and Gamut) bought up $600 million of the loan.

Without necessarily singling out SSB, Apollo’ strategy was par for the course in this era’s market environment:

Apollo’s $25 billion private equity fund has shifted “almost entirely” to a distressed strategy under which it aims to gain control of companies by investing in their debt… Right after the “market dislocation” thirteen years ago, Apollo’s private equity fund VII was two-thirds invested in distressed, he said, compared with less than five percent for its next fund. “That is the bandwidth vis-à-vis distressed-for-control that can come out of the private equity funds.”

A Modest Proposal to Get J. Screwed

Just three months after purchasing SSB’s debt, Apollo attempted to activate the trap door against SSB. This collateral-stripping maneuver was popularized by a number of high-profile cases — first made famous by J. Crew, but it also transpired in iHeartMedia, Petsmart, Revlon, Neiman Marcus, Travelport, Cirque du Soleil, and so on. SSB barely missed the list.

How J. Crew earned the title in 2016:

[J. Crew] put its brand name and some other intellectual property into a new entity in the Cayman Islands that was beyond the legal reach of its existing lenders. Then it used that new entity to borrow $300 million from Blackstone Group LP. The existing lenders, who saw valuable collateral disappear before their eyes, cried foul, but J. Crew argued that its move was perfectly legal under terms of the loan documents. (The issue was never litigated.) Since then, lenders to other companies have worried about being “J. Crewed”—i.e., victimized by a deal that siphons away collateral backing their loans. It rhymes with another word.

What Apollo proposed to SSB was a textbook example of just that. From the court filings:

Led by late-comer behemoth Apollo, which only first purchased its Serta debt three months ago at deeply discounted trading prices, these Plaintiffs have spent the better part of the past three months engaging in an elaborate scheme to strip away the other First Lien Lenders’ Collateral for their sole benefit. In these trying times, Serta finds itself facing a liquidity problem, and these Plaintiffs tried to take full advantage of Serta’s plight. They proposed a predatory financing transaction to rip away Serta’s “crown jewel” trademarks for the nationally recognized Simmons/Beautyrest and Tuft & Needle mattress brands (worth at least hundreds of millions of dollars) into a subsidiary outside the reach of all other First and Second Lien Lenders’ claims that would have secured Plaintiffs’ own new structurally senior facility alone.

Apollo would take the “crown jewel” IP assets, being used as collateral for secured loans, and move them into a newly created subsidiary. Then that subsidiary would borrow new money. This would allow Apollo to strip the collateral being used for existing loans and kind of double-dip with it.

In exchange, Apollo dangled the carrot of operating capital, knowing that runway was running out for SSB. (So predatory.) All SSB had to do was agree to siphon away the brand IP of Serta, Simmons, Beautyrest, and Tuft & Needle for the exclusive benefit of the Apollo-led creditor group.

While this would have provided strong, prioritized collateral for Apollo’s new loans, it would have left the other lenders hanging dry with the full amount of their original loans but with much less collateral. The newly formed subsidiary, rather than the original borrowing entity, would hold the valuable assets instead.

Granted, doing this dirty deal would have provided a temporary cash infusion to SSB, but would it ultimately have been worth the trouble? Not to mention, the new loans taken out by the subsidiary would lead to an overall increase in total debt load for the company.

Creditor-on-Creditor Violence

Apollo’s J. Crew maneuver against SSB could have and should have worked. But it was foiled by the other majority lenders (Eaton Vance, Invesco, Credit Suisse) with a counter-proposal to the company that pulled the rug out from under Apollo.

(If my own brand, Tuft & Needle, were not wrapped up in the middle of this, the utter absurdity may be kind of entertaining. But it is, so I must say it is all stupid games.)

Bloomberg’s Matt Levine shared an illustrative example of the judo move by Advent and Eaton Vance against Apollo:

A company borrows $1 billion, in a syndicated loan or a bond issue, from a bunch of different investors.

As is customary, the loan agreement or bond indenture says “this agreement may be amended by a majority of the investors.”

Time passes and the company runs into some trouble.

The company goes out to 51% of the investors — holders of $510 million of the bond or loan — and says: “Psst. We will pay you back 110 cents on the dollar — $561 million total — if you agree to let us stiff the other guys.”

So the 51% holders vote to amend the agreement to say “these holders will get 110 cents on the dollar, and the other holders will get zero.”

The other 49% are really mad and surprised.

The amendment works, 51% of the holders make a nice profit, 49% of the holders lose all their money, and the company pockets the extra $439 million.

Even though the initial exploit failed, Apollo was unwilling to accept defeat. This has now become a battle between heavy-hitting creditors. The stakes are high and the consequences of defeat could be catastrophic for the portfolio returns (and egos) of either side. In 2020, Apollo incited litigation still ongoing to this day, and as the tension reaches its climax in 2023 — with SSB now facing bankruptcy — it is yet unclear which side will emerge victorious.

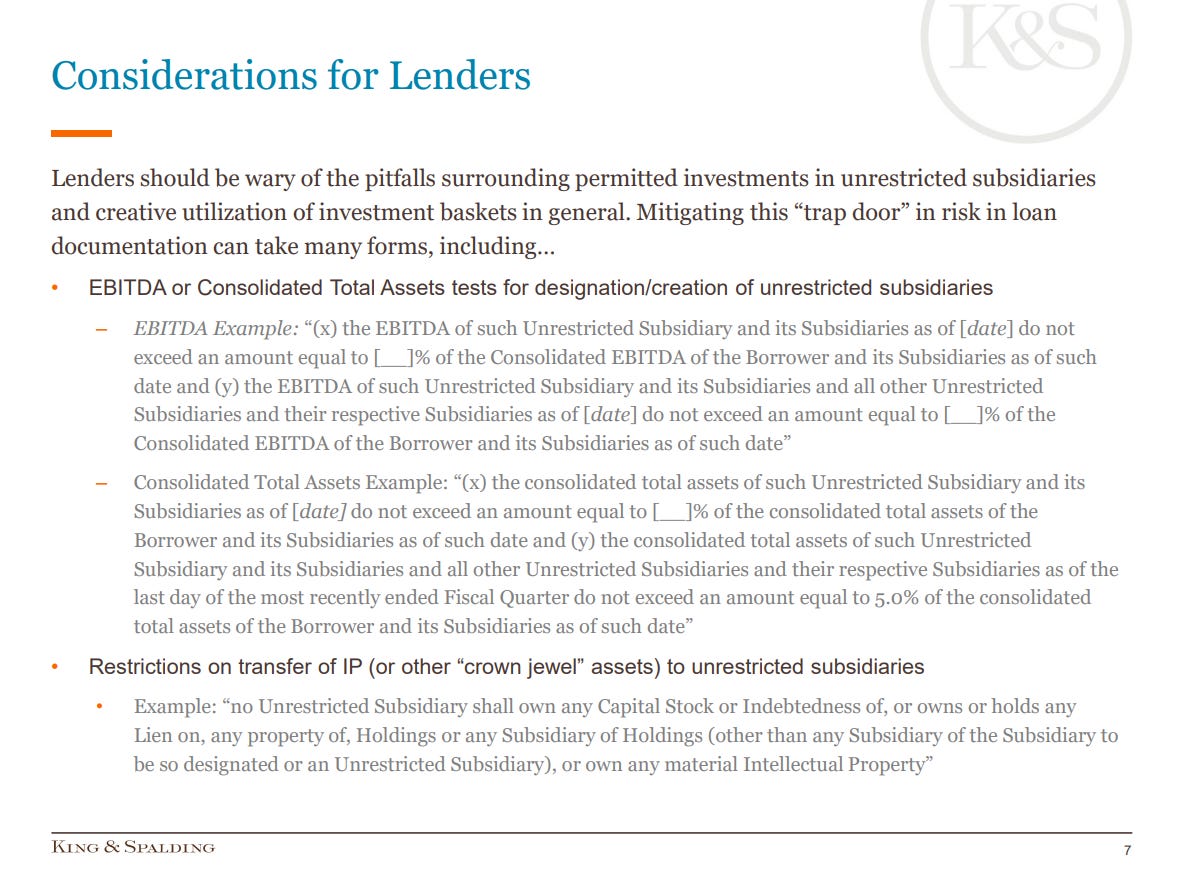

Distressed debt investors have a fast-growing bag of tricks to take advantage of situations like this. It’s a bit of a cat-and-mouse game, where high-powered lawyers scour through creditor agreements and look for creative ways to activate new “trap doors”.

Once a trap door is used and publicized, though, it is pretty much burned since the lender community will patch future contracts. There’s already a ton of legal literature around “J. Crew blocker” provisions:

As we enter 2023 with a downturn economy, we will see an increased exploitation of loopholes in creditor agreements like this in the overall market. As a result, companies like SSB get squeezed for blood from all directions: from the dwindling economy and the company’s own cap table using the business as a battleground for control and profits.